Safe haven buying is helping drive gold and silver steadily higher this week. Silver in particular is looking strong as the weekend approaches, having gained more than 7% in the past week.

Despite the pullback from recent all-time highs, demand for gold remains strong, and the metal has set up a healthy level of support at $2,300/£1,840. Having only slipped below these levels briefly in the past fortnight, gold is holding onto these historic high prices, in a positive sign for the metal.

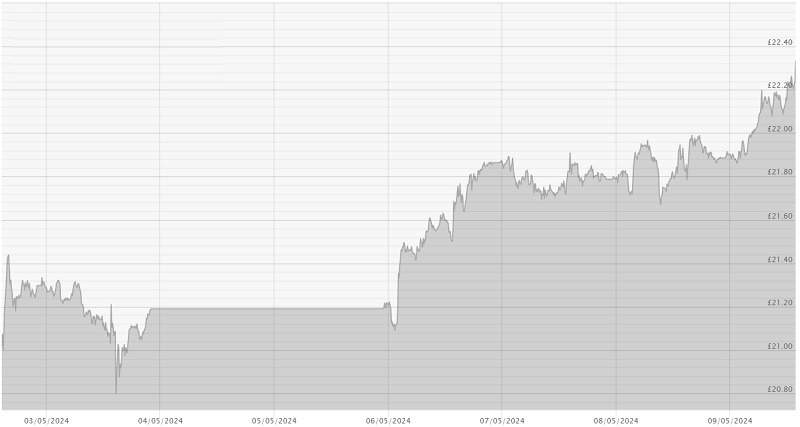

Silver is proving the star of the show this week however; gold has gained 2.5% since hitting a low of £1,813.15 last Friday, but silver has increased by an impressive 7.2% in the same period. Having hit $27.97 this afternoon, $28 will be a key level of resistance, and a close above that level for the weekend will be extremely positive for the price of silver.

Today has seen some currency volatility surrounding the Bank of England’s latest rate meeting. As expected, the BoE kept UK rates unchanged at 5.25%, but the vote saw two members (of the nine-member committee) call for a rate cut. The BoE has looked more dovish at recent meetings and suggested that June could see the first UK rate cut, and that the bank may cut rates further than current market expectations.

After initially dropping, the pound has actually found itself up on the day so far due to a slip in the US Dollar Index following higher-than-expected US jobless claims.

Markets are still faced with plenty of uncertainty in the world. Some indicators suggest a global economy that has held up to a period of higher rates, and that inflation is tamed. Other suggest a global slowdown is just beginning, and more will be needed to bring inflation under control. Big tech companies like Microsoft continue to lay off large numbers of staff, Japan’s Yen is in an ongoing currency crisis, and the wars in Ukraine and Middle East show no signs of resolution.

Gold and silver’s continued strength as we head into the normally quieter summer months leave both metals well poised to push higher in the second half of 2024.