The World Gold Council has released its 2022 Outlook and is expecting another year of mixed fortunes and forecasting for the precious metal, though the short-term concerns may turn out to be a blessing for gold.

According to the WGC, “Near term, the gold price will likely react to real rates in response to the speed at which global central banks tighten monetary policy and their effectiveness in controlling inflation.” This reflects what we already saw with a stock market response to register record highs in recent weeks for all the major western exchanges, but it doesn't tell the full story.

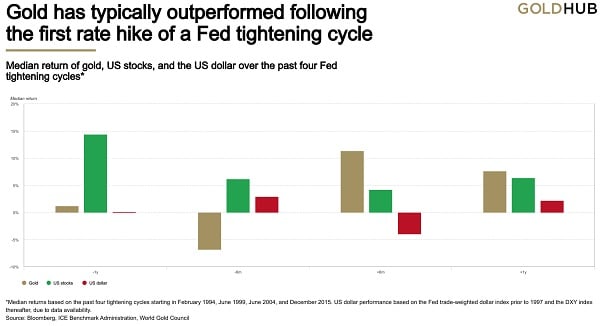

As shown by the chart below, historically speaking the impact of rate hikes produces limited headwinds to hinder gold and if anything the difficulties subside and gold enjoys a strong six month period.

Image courtesy of the World Gold Council

Image courtesy of the World Gold Council

Read more at https://www.gold.org/goldhub/research/gold-outlook-2022

Part of the reason for this appears to be that major central banks, such as the Federal Reserve, make a bigger noise about tightening monetary policy than the resulting action. The bark is nastier than the bite, but the results have typically hurt the US dollar – and benefited gold in the process.

The other big point the Council makes is the risk of 'elevated inflation' and 'market pullbacks'. We're all experiencing inflation, and some are still sticking to their guns that its transitory. This conflict is another factor helping stir up safe haven asset demand. Add in the issue of market pullbacks, relating to new Covid variants, supply chain issues, and a tricky labour market, and you have three big factors that can suddenly trigger a market shift. It's no surprise then that gold has performed well in these instances as a liquid asset.

The final point of interest, and something we'll definitely touch upon later in the year, was central bank gold demand. This was the driving factor for gold's price gains in 2018 and 2019, and likely would have been the same in 2020 and 2021 were it not for Covid. The obvious answer is that banks would like to get back to investing and diversifying their reserves away from a specific currency, but whether that becomes viable with the pullbacks is one challenge and then, even if it does, will the appetite be there? Or will everyone be too distracted with risk-on assets to remember to protect themselves?